Editor's note: Seeking Alpha is proud to welcome Zorko Investments as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to the SA PRO archive. Click here to find out more 禄

We believe that QIWI Plc (QIWI) is overvalued. QIWI is a Russian company that trades on the Nasdaq. We see that many investors have a poor understanding of the company's processes. QIWI is losing out due to the competition of major players. It is highly dependent on one business line, which is has regulatory and competitive risks. Below we will provide our point of view on QIWI.

No core competence to win in a tougher market

In their 20-F SEC filing, QIWI admits that competition will negatively affect the company's market position:

As major commercial and retail banks increase their online and virtual presence and come up with increasingly sophisticated products directly competing with our core competencies, our competitive position could be severely undermined, resulting in reduced demand for our products, both with respect to our payment services business and the other financial services projects that we are pursuing.

Let's look at QIWI's e-commerce segment. In 2017, the e-commerce segment net revenue comprised 51% of company's total net revenue. According to Credit Suisse research on QIWI from April 7, 2017, 85% of QIWI e-commerce payments come from betting, gaming, and social networks. But the number of payment options for a customer continues increasing as new players enter the market.

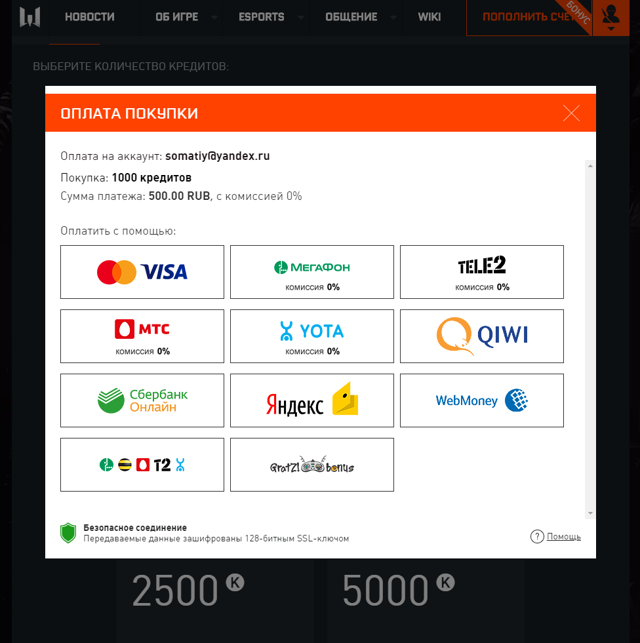

Here is an example: the online gaming industry. Mail.ru estimates online gaming market in Russia to be ��56.7bn in 2016 ($0.9bn) with a CAGR of 24% over the last five years; according to our estimates, Mail.ru controls about 50% of this market. In 2017, mobile operators Megafon, MTS, Veon, Tele2, and Yota started to fight for players' payments and even canceled commissions. Here is Warface by Mail.ru's payment page, and today players have 11 different options to pay for their purchase: Source: Warface

Source: Warface

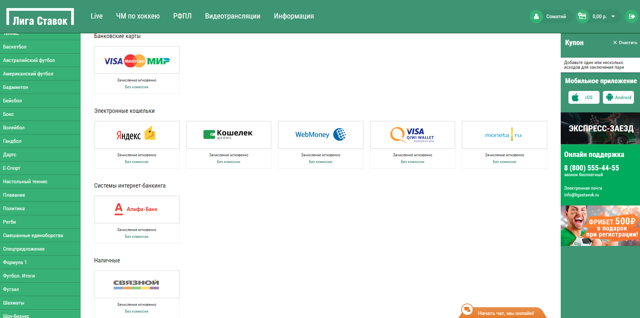

Below is a screenshot of a payment page from Liga Stavok, which controls 9.3% of the Russian offline sports betting market and is the third most visited betting website in Russia:

Source: Liga Stavok

A player has eight different options to make a no-commission payment, including the following:

By card: 90.6% of all Russian internet users have at least one bank card By Yandex.Money, a Sberbank-controlled company with 59.5% e-wallet market share vs. QIWI's 53.7% By Alfa-Bank online banking, the third largest bank by the number of debit card users By cash in Svyaznoy stores, an electronics retailer, and payment processing company with 2,800 stores in virtually every mall in Russia

By the moment of payment, most consumers will have money in their bank account or in their mobile phone account. Making a payment does not require them to take any extra actions. To pay via QIWI, a consumer has to take extra actions.

Retail banks and mobile operators own an "ecosystem" that their customers use on a daily basis and is where they keep the money. QIWI's main disadvantage with regard to competition is that they are nothing but a payment company. We believe that increasing competition will inevitably result in the payments yield's decline and in QIWI's market share drop.

High dependence on betting and online games

On April 24, 2018, JPMorgan published some research on QIWI. In their research, JPMorgan refers to their Q&A session with QIWI's CEO, CFO, and IR as sources. According to them, 7.5% of all QIWI payments, or 40% of e-commerce payments, currently come from the betting industry. In fact, QIWI is doing a great job in betting: They became one of the two largest Interactive Bets Accounting Centers, set up with the association of bookmakers in Russia.

QIWI believes that their share in this market may exceed 50% in the next two to three years, up from the current 20%. And industry growth of 25% per year is forecast. According to Reiting Bukmekerov research, the current size of Russian sports betting market is ��403bn ($6.5bn), and the potential for this market is ��1'200bn ($19.3bn). Their estimates seem accurate when compared to QIWI's statements. With 25% annual growth, it will take the market five years to reach this level. If this happens, QIWI will increase their net revenue from betting to $289mln in five years - four times what it is now.

By our calculations, based on JPMorgan research and QIWI's 2017 financial statement, betting contributes 16% to company's total net revenue (��2.1bn of ��12.6bn). Betting net revenue compared to IFRS net profit is 67%.

We trust QIWI's estimates and believe that the company has the potential to increase their betting market share. However, we see legal risks, which will be discussed below. In emerging markets, it's usually fine when one of the business lines is at legal risk. But in this case, it is their main business line.

Government risks

QIWI has an advantage that often helps it leave competitors, such as retail banks, behind and requires customers take a few extra actions to pay via QIWI. This advantage is anonymity of payments. QIWI is not a bank and does not have legal obligation to identify its customers. Payments up to ��40,000 per month (higher than the average monthly salary in Russia) can be made after registering with a phone number only, which means anonymously.

From our research, this has three use-cases:

Use-Case 1: Betting, gaming, and online casinos. As per Russian tax code (Part 2, Article 228), a physical person is responsible for tax declaration and payment on winnings up to ��15,000 - 40% of an average Russian's monthly income. QIWI leaves space to let players win and stay anonymous, hence avoid taxes. Use-Case 2: JPMorgan's report says that QIWI is an attractive platform for the self-employed, such as tutors and personal trainers. QIWI identifies such accounts and charges them a fee for P2P transactions. This does not comply with Russian tax code, by which such citizens are subject to tax accounting. In fact, such transactions are often used by criminal entities; QIWI P2P transactions are a cheap way to anonymously buy/sell cryptocurrency in Russia. Use-Case 3: According to Rosstat, 1.543mln migrant workers legally worked in Russia in 2016. According to Federal Migration Service information provided for MIR24 in 2016, about 1.5mln migrant workers work in Russia illegally. Of those, 99.9% come from CIS countries, where QIWI operates a chain of payment terminals. Legal and illegal migrant workers use QIWI wallets to transfer money to their home countries, and they need anonymity to avoid taxation.

Proposals to completely prohibit anonymous e-wallets are being raised by government officials in Russia. In January 2018, it was reported that the CBR, Rosfinmonitoring and the Ministry of Finance are actively discussing newly proposed legislation that would ban the use of anonymous e-wallets completely, or at least prohibit the reloading of such e-wallets other than from a bank account. Russian lawmakers normally demonstrate scrutiny in matters of anonymous use of the internet. A very recent example is the ban of Telegram, which was executed within a matter of days.

QIWI is a company that exploits legal arbitrage opportunities in Russia, and the government is not OK with it. Therefore, we believe that there is a strong legal risk for QIWI's business. Another question is this: If QIWI has to identify all of their clients, how many will choose QIWI to top up their betting account next time?

Currency risks

QIWI's stocks are traded on the Nasdaq and their price is quoted in U.S. dollars, while they process payments in Russian rubles. We expect the ruble to decrease vs. the dollar in 2018, and QIWI is exposed to this rate change.

Suspicious CEO share increase

On April 27, 2018, Sergey Solonin (QIWI CEO and main owner) borrowed money from Credit Suisse to buy Kirill Evdakov's (QIWI co-founder) stake. Solonin bought 495,423 Class A shares at the price of $15.72.

There are two types of shares in QIWI Plc:

Class A - gives the holder 10 votes Class B - gives the holder 1 vote

Both A and B class shares receive the same dividends. The shares in free float are Class B shares, and on April 27 their price was $18.11. This means that Solonin bought shares that give 10 times the control of Class B shares at a price 13% lower than the market price of Class B shares.

Kirill Evdakov could have sold his shares to anybody at the market price, but chose to sell them to Sergey Solonin at 13% cheaper than the market and receive $1.2mln less for the deal than he could of gotten. We believe that this is a bearish signal. Evdakov agreed to sell shares cheaper than market only if he believed the market wouldn't buy this many shares. Solonin already had a 59.44% voting interest in QIWI, and this deal cannot be explained by his desire to get more control over the company. Solonin agreed to buy Evdakov's shares because there were no other buyers and he feared that the sale could result in a price drop.

Downside potential calculation

We made a DCF model for this stock, and we believe QIWI is 42% overvalued. Fair price of the company is about $650mln (currently it's $1,123mln), or $10.67 per share. Our valuation does not include regulation and currency risk, which we believe will have a negative impact on the share price.

When we see a downside potential for a company, we usually stay neutral or recommend selling it. But in this case, our recommendation is to go short QIWI.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

UGAIN (CURRENCY:GAIN) traded flat against the U.S. dollar during the 1 day period ending at 23:00 PM E.T. on June 22nd. One UGAIN coin can now be purchased for about $0.0023 or 0.00000037 BTC on popular cryptocurrency exchanges including YoBit and CoinExchange. During the last week, UGAIN has traded up 59.4% against the U.S. dollar. UGAIN has a total market cap of $0.00 and approximately $2.00 worth of UGAIN was traded on exchanges in the last 24 hours.

UGAIN (CURRENCY:GAIN) traded flat against the U.S. dollar during the 1 day period ending at 23:00 PM E.T. on June 22nd. One UGAIN coin can now be purchased for about $0.0023 or 0.00000037 BTC on popular cryptocurrency exchanges including YoBit and CoinExchange. During the last week, UGAIN has traded up 59.4% against the U.S. dollar. UGAIN has a total market cap of $0.00 and approximately $2.00 worth of UGAIN was traded on exchanges in the last 24 hours.